It Could Be Said #24 Britain Needs An Anti-Inflation Strategy

The problem with Rishi Sunak's Spring Statement was not that it did too little, but what it did is likely to be harmful

Rishi Sunak has an odd trick of delivering financial statements that manage to be more aggressive than initially expected, dismissed as underwhelming upon closer consideration in the days and weeks immediately after the announcement, and then ultimately considered too generous in the fullness of time. We saw this repeatedly during the pandemic when he would be dragged to the House of Commons to deliver a budget-busting package of measures that would shock those watching live for its largesse, then irritate people doing secondary analysis for failing to grapple with the full breadth of the problem, only to be ultimately accused of wasting money.

That cycle has occurred unusually rapidly with the Spring Statement; the initial reaction to the Chancellor spending billions to not only cut fuel duty by 5p but cut VAT on fuel efficiency home improvements and lift the National Insurance threshold was genuine shock that he had gone far further than the pre-briefings suggested. But by the end of the night people had realised his measures would not make a dint in the squeeze hitting British households, despite costing billions.

And in the fullness of time, we will realise that his biggest mistake was spending too much money, not too little.

Hello Inflation, My Old Friend

It is curious that the Tories have ceded the battlefield to Labour to such an extent that the crisis is being billed as a “cost of living crisis” rather than what it actually is - the alarming signs that we’re at the beginning of an inflationary spiral.

There are two dimensions to this. The first is the one that most people are familiar with; the coronavirus pandemic and now the war in Ukraine has caused a supply shock which has reduced or complicated the supply of key items, so pushing the price up. This has been exacerbated by behavioural changes caused by lockdown causing demand to explode or implode for various items, which has made it difficult for companies to predict what is and isn’t wanted. This was the side of inflation that once reassured people that inflation would prove to be transitory, because as soon as supply and demand returned to its pre-pandemic norms then everything would surely be fine.

I believed this too but the persistence of high-inflation has clearly proven me and my fellow inflation doves wrong. This is partially because we underestimated how long the shocks would continue, something not helped by covid mutations and China’s inability to move beyond Zero Covid. Likewise, the War in Ukraine means that the supply chain issues are actually poised to get even worse, especially in key sectors such as fuel, energy, fertiliser, and food.

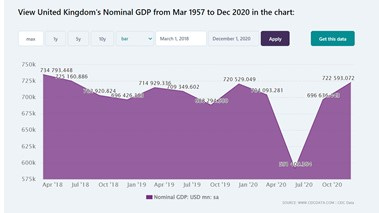

But what makes this commodity inflation all the more concerning is that we also have too much money sloshing around in the economy. If you look at Nominal GDP, that is Gross Domestic Product without any attempt to account for inflation, you see that the aggressive intervention the Government made to mitigate the economic consequences of lockdown has successfully ensured that economic activity rapidly bounced back to where it was before the pandemic. It will almost certainly keep expanding, and we may well hit the point this year when there’s more cash in the economy than ever before.

More money in the economy when there’s fewer good is a dangerous combination. If people have spare money to hand, which many people do due to furlough and lockdown blocking them from spending money as they normally would for much of 2020 and 2021, then they will accept higher commodity prices rather than haggling or waiting the supplier out. Businesses then realise that they can charge higher prices without being penalised by consumers, so encouraging them to be more aggressive with their price hikes. This may lead to some workers demanding pay increases to allow them to buy the products available, pay increases that businesses may either have no choice to allow, or be comfortable allowing because they believe the widespread price inflation makes it easier to pass on the costs to the consumer. Ultimately the consumer notices that prices are consistently going up, and so rather than responding to an unexpectedly high price for an item by refusing to purchase it in the expectation it will cost less the following week, they rush to buy it out of fear it will soon cost more. At that point, more workers who can, will start demanding higher wages from their employers, wage increases that may again be passed onto consumers. And so the cycle continues...

This is an inflationary spiral, where people respond to price increases in logical but ultimately self-defeating ways. And all Rishi Sunak did with the Spring Statement was half-heartedly throw some fuel on the fire by subsidising people’s consumption of…erm..fuel.

PULL THE BLOODY CHAIN

A common refrain over the past year is that the surge in prices can be resolved by supply-side reforms i.e. deregulation, investment in onshoring, increased immigration, increased oil and gas production by Western countries, etc. The problem with this approach is that much of these improvements whilst welcome, would take a while to be implemented let alone have an impact on prices. It’s also worth noting that persistently high inflation is also likely to cause further supply shocks; one of the reasons energy costs are increasing so much in the UK is that our market is imploding, with many newer suppliers being driven out of business.

The only way to stop inflation running out of control is to cool the economic down, otherwise you inevitably have too much money chasing too few goods. Luckily there’s a very simple way to cool the economy down - have the Bank of England induce a recession by increasing interest rates. This is what America’s Federal Reserve famously did under Paul Volcker. Whilst as a non-monetarist I would reject the idea that such measures solved inflation for ever, they do create time and space to address the issues in supply chains.

The only problem is that the necessary increase in interest rates would be incredibly painful. Noah Smith quoted macroeconomist Olivier Blanchard’s belief that you need interest rates to be double the core inflation (i.e. minus fuel and food) rate if they’re designed to bring the economy to heel; in Britain that would require interest rates of around 10%. That would be a more than a 1000% increase and their highest level since the early nineties. Such a dramatic increase in the cost of borrowing would see a wave of bankruptcies and repossessions, as the finances of both individuals and companies are blown apart due to increased borrowing costs. It would also certainly provoke a level of unemployment that we have not seen since the last tightening of the money supply in the 1980s. Indeed, the human misery caused may be higher still given how much more reliant British households are on debt than in the 1980s.

I Wouldn’t Start From Here

Whilst there are no ways to avoid some economic pain, there are three possible ways to avoid the Bank of England inducing a recession or the economy being ovewhelmed by high inflation. The first is to again hope that the supply-chain disruptions prove temporary and that the flow of cheap fuel from Russia and the flow of cheap good from China shortly resumes. Neither seems likely, or even welcome. The second is to hope that people and businesses can learn to adapt to inflation in ways that don’t provoke an inflationary spiral. The signs that people are drawing down savings and businesses aren’t passing on the Chancellor’s tax cuts, shows that isn’t likely.

That leaves the third option. If we don’t want the Bank of England to cool the economy down, then the Government needs to do the deed itself. This is indeed what Margaret Thatcher’s first government did, with Geoffrey Howe using a combination of public spending cuts and tax rises to induce a recession that significantly reduced inflation1.

But whereas interest rate rises are blunt tools, changes to tax and spend provide a wider array of measures, which (unlike in the 1980s) can be used in ways to focus the pain on those who can most afford it. The Government could for example pair tax rises for the rich and middle class, with an increase in universal credit to support the poorest households. Maybe the tax system could be tweaked to coerce the affluent to save rather than spend, which whilst not taking money from them, would still help cool the economy down. Likewise an increase in Corporation Tax, changes to VAT or even Windfall Taxes on certain sectors could discourage companies from profit gouging, with some of the proceeds being redirected into investment to solve the supply chain issues.

Of course the problem is that such measures would be hideously unpopular. To work they would have to more than balance out, with the Government taking money out of the economy. But people like having money, and they like spending it, and so would resent a Government who openly said it was increasing taxes to thwart these desires. That is basically why central banks were given their independence in the first place - it seemed easier for politicians to let bankers take the difficult decisions than make them themselves.

But that lack of responsibility was always an illusion; ask Gordon Brown if people tolerated him saying it was the bankers’ fault the economy imploded in 2008. The people hold their democratically elected leaders responsible for the economy, irrespective of whether that’s fair or not. Rishi Sunak should remember that if he wants to stay living in Downing Street beyond 2024.

Typically today’s Thatcherites forget the important role that tax rises played in Thatcher’s economic strategy